Risk Management in Algorithmic Trading Systems

Risk management in algorithmic trading is not about predicting losses — it is about enforcing predefined constraints that limit exposure, control failure scenarios, and prevent uncontrolled behaviour.

This page explains how risk management is designed and implemented as a core system layer within algorithmic trading infrastructure.

Why Risk Management Is a System Component

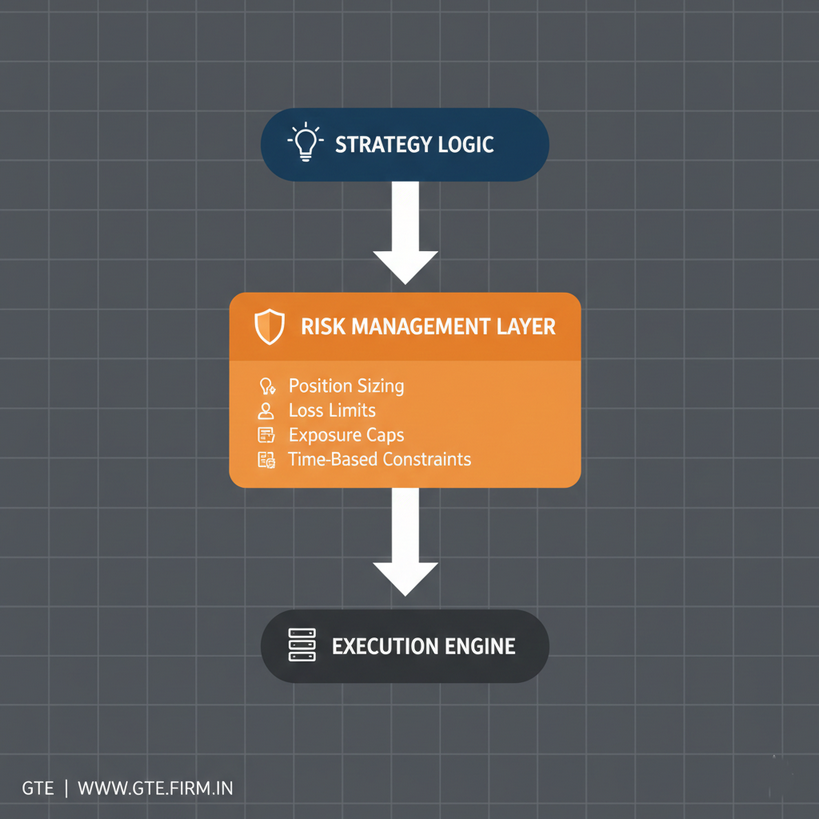

In algorithmic trading, risk management cannot be added after strategy logic. It must exist as an independent enforcement layer that operates regardless of market conditions or signal confidence.

Well-designed systems assume that:

- Strategies will fail periodically

- Market conditions will change unexpectedly

- Execution issues will occur

Risk management exists to ensure that these failures remain contained.

Types of Risk Addressed by Trading Systems

Algorithmic trading systems typically manage multiple categories of risk:

- Market risk – adverse price movement

- Exposure risk – excessive position size or concentration

- Execution risk – slippage, rejections, partial fills

- Operational risk – system errors, connectivity failures

- Behavioural risk – overtrading, revenge logic, parameter abuse

Each category requires explicit handling through rules and constraints.

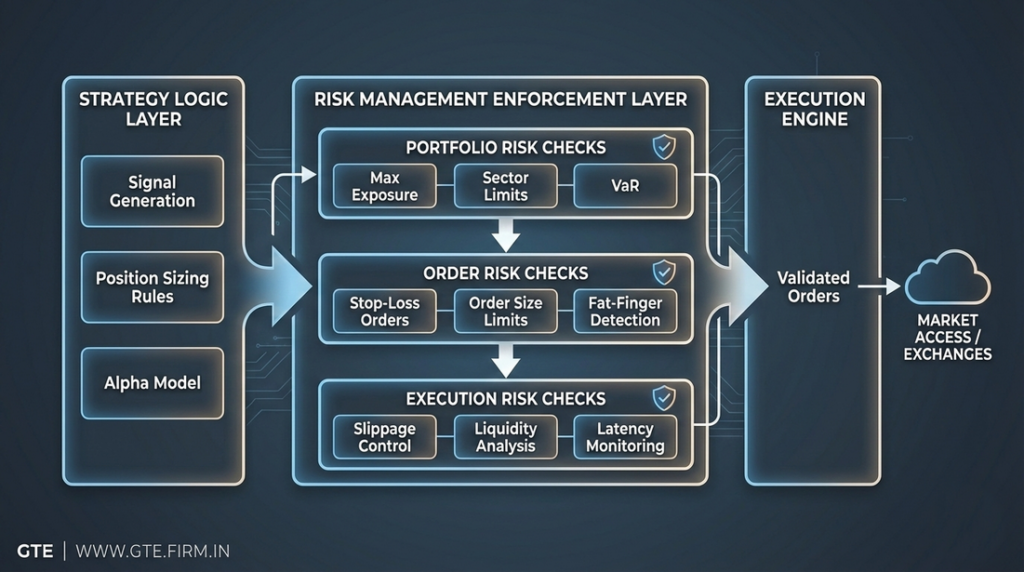

Core Risk Controls Used in Algorithmic Systems

Position Sizing Controls

Position sizing rules define maximum allowable exposure per trade, instrument, or strategy.

These controls may be based on:

- Fixed quantity limits

- Capital percentage allocation

- Volatility-adjusted sizing

The system enforces limits; it does not decide whether a trade is “good”.

Loss Containment Mechanisms

Loss controls define when activity must stop.

- Per-trade stop conditions

- Daily or session-level MTM limits

- Strategy-level drawdown caps

Once breached, the system restricts further action regardless of signal state.

Time-Based and Session Controls

Risk is also managed through time constraints.

- End-of-day (EOD) position closures

- No-trade windows

- Market session filters

These rules prevent exposure during periods of elevated uncertainty.

Monitoring, Alerts, and Auditability

Risk management systems must be observable.

Common monitoring features include:

- Real-time exposure tracking

- Threshold breach alerts

- Execution status logging

- Error and exception reporting

Alerts inform operators — they do not override enforcement logic.

Separation Between Strategy and Risk Logic

A critical design principle is separation of concerns.

- Strategies generate intent

- Risk systems enforce limits

- Execution engines place orders

This separation ensures that no strategy can bypass predefined constraints.

Risk Management Is Not Advisory

Risk management systems do not:

- Recommend trades

- Predict outcomes

- Guarantee protection

They simply enforce boundaries defined in advance.

Where This Page Fits

This page focuses on risk enforcement within algorithmic trading systems.

For system design context, refer to:

Algorithmic Trading Development Process →

For conceptual grounding, start with:

Introduction to Algorithmic Trading →

Risk is controlled by rules, not confidence.